A growing number of companies are offering student loan repayment assistance programs as an employee benefit. In fact, the number of employers offering student loan-related benefits doubled to 8% over the past year, the 2019 Employee Benefits Report by the Society of Human Resources Management (SHRM) found.

There are two primary reasons employers are increasingly partnering with student loan assistance vendors to provide this benefit. First, employers realize financial concerns and student loan debt continue to be significant drivers of stress in the workplace. Second, with low unemployment rates, employers are looking for new strategies to gain a competitive edge in recruiting and retaining employees.

Student Loan Benefits Come in Various Forms:

- Employer serves as advertising arm of refinancing company.

This option is for employers who realize student loan debt is an issue but do not want to budget assistance for their employees. The employer simply provides information on organizations that provide consolidation and refinancing for student loans. They essentially act as an advertising arm of the refinancing companies: “You can go here to refinance your student loans at a potentially lower rate.”

Employer Investment: Minimal time in making the information available.

- Employer provides educational services on eliminating student loan debt.

Working with a preferred student loan assistance vendor, the employer provides access to educational resources on financial planning and eliminating student debt. While these services often include refinancing options, they also provide alternatives to refinancing that may make more economical sense for the employee.

Employer Investment: Typically includes either a monthly fee per employee (PEPM) or per participant (PPPM).

- Employer contributes toward employees’ student loan debt.

There are several ways in which an employer may contribute financially to reducing their employees’ student loan debts:

-

- Monthly contribution toward debt. To reward longevity, some employers will increase this amount each year. For instance, during the first year of employment, the employer may contribute $50 a month toward the employee’s debt, and then increase the monthly payment by $25 each year, up to an annual maximum.

- Employer match. Some vendors will design a program where the employer matches employee contributions (up to a maximum amount) toward retiring their debt.

- In lieu of 401(k) contributions. Under this plan, the employer contributes to the employee’s 401(k) an amount equal to the employee’s payment toward their student loan.

Employer Investment: In addition to the amount contributed to the employees’ debt, the vendors will charge either a monthly fee per employee (PEPM) or per participant (PPPM).

Free vs Fee

Employers desiring to offer student loan assistance to their employees will often question the fees charged by vendors. Therefore, the question must be asked, “What does the employer get by partnering with a student loan assistance vendor that charges a fee?”

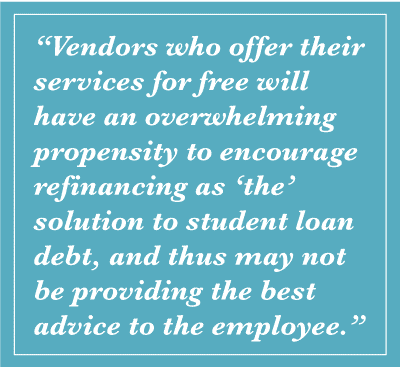

Understanding how a student loan vendor generates revenue may shed light on the type of service they offer. Vendors who do not charge for their services are most likely the bank providing refinancing, or a third party receiving a referral fee and/or a percentage of the interest or refinance fees. These vendors will have an overwhelming propensity to encourage refinancing as “the” solution to student loan debt, and thus may not be providing the best advice to the employee.

Vendors who charge a fee are more likely to offer enhanced services to both the employer and the employee. Instead of pushing refinancing as the first option, these vendors will provide educational resources to help the employee make wise financial decisions regarding their student loans.

Some of the services provided by vendors who charge a fee may include:

- Financial education and student loan counseling

- Information about, and assistance with, student loan forgiveness for employees working with a non-profit

- Employer matching repayment plans

- Option of employer payments directly to student loan services

- Payroll deduction and the ability to run contributions through payroll

- Ability to provide options for co-signers (parents)

- 529 college savings plans

- Technology and mobile apps

It should be noted that some vendors who charge a fee may receive additional revenue through refinancing. Therefore, it is important to ask the vendor if they derive any income from the refinancing of loans.

The Benefit Company Can Help

Selecting the right student loan vendor depends on the needs, desires, and demographics of the employer.

We would like to help.

Contact your Account Executive or Consultant at The Benefit Company. You can rely on our expertise to guide you through the selection process. By answering just nine quick questions we help you begin the journey to find the best solution for your student loan assistance needs.

Director of Population Health & Wellbeing

- Population Health

- Employee Wellness & Wellbeing

- Human Resources